Most scientists who become founders learn the hard parts in the middle of a deal they were not prepared for. A term sheet that does not fit the structure they built. A cross-border investor with expectations nobody explained. A product that needs to be redesigned, not relabelled, to work in a new market.

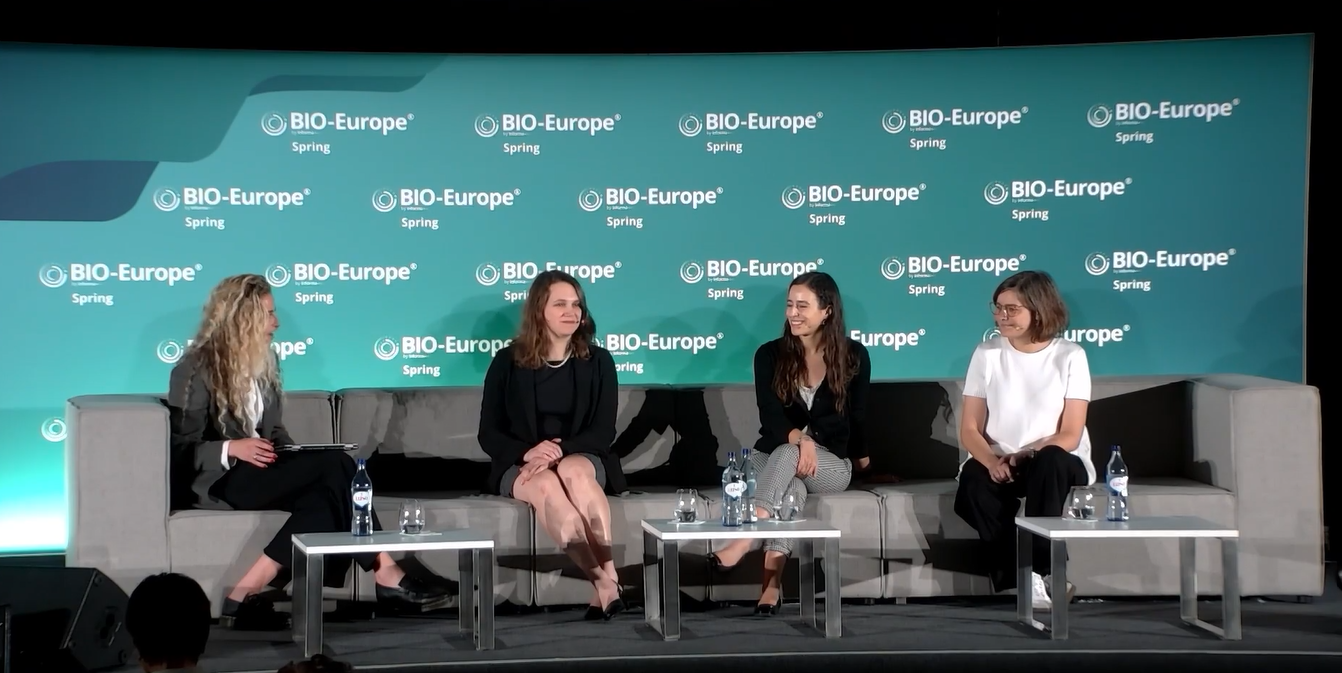

The panel “From Seed to Scale: Women Leaders on Raising Capital and Scaling Globally in Digital Health and Life Sciences” at OBIO’s International Women’s Day Celebration was a chance to hear it before that moment arrives. Founders, investors, and legal experts who had been through it, talking plainly about what the experience is actually like.

You do not need to be raising a global round for this to be useful. You just need to be building something.

The early decisions are the ones that cost you

Most founders think about legal structure exactly once. Usually when someone puts a document in front of them.

The panel pushed back on that quietly but firmly. Where you incorporate, how IP is assigned, how equity plans are structured for international hires. Each decision feels administrative when you make it. Each one can become a real constraint years later when you are trying to bring in a foreign investor or open a subsidiary in a new market.

“The biggest challenge that I see is where companies make very early decisions which, unfortunately, are very difficult to unravel.”

The consistent advice: get legal and tax counsel before you hire internationally, before you take cross-border capital, before you sign anything with a foreign partner. Not after. The cost of early advice is small. The cost of fixing a bad structure later is not.

On whether to redomicile or build subsidiaries, there is no universal answer. One path on the panel was moving headquarters to Ireland to qualify for the European Innovation Council, which can fund up to seven million euros. Another was keeping the Canadian parent and building subsidiaries in target markets to protect IP flow and control. Both are legitimate. Both require real counsel before the decision, not during it.

Investor relationships are longer than they feel at the term sheet stage

The panel talked openly about co-investment with sovereign funds and European partners, and the European Innovation Council came up more than once as a genuinely strong vehicle. The enthusiasm was real.

So was the caution.

“It’s a marriage. It is nearly impossible to get an investor off the cap table.”

Strategic investors, corporate venture arms, sovereign funds, state-backed programs, they come with expectations that passive financial investors do not. Longer diligence. Different instruments. Often a board seat as a condition of investment. And a board seat at a startup is not symbolic. It is a governance shift with real consequences for who makes decisions about the company.

The other question worth sitting with before any term sheet: what does this investor actually open for you beyond the capital? Market access, clinical networks, regulatory credibility, payer relationships. Capital that opens doors is worth more than passive capital at the same valuation. The work is figuring out which one you are actually getting.

Budget for the legal costs nobody tells you about

Someone put a real number on the table.

Legal fees over $200,000, not to close a cross-border round, but just to determine whether it could be closed. It was not a complaint. It was a heads up for everyone in the room who had not been through it yet.

Cross-border deals in the Middle East and parts of Asia involve multiple legal teams, extensive documentation, and diligence processes that look nothing like what North American founders are used to. Sophisticated foreign investors often expect governance mechanisms that Canadian companies have to

build from scratch, because the standards they know are simply different.

This is not a reason to avoid global capital. It is a reason to go in with clear eyes about what it costs to pursue it.

Expansion is a product decision, not a sales one

The founders on the panel who had scaled internationally without rebuilding everything shared a common thread. They had built for it before they needed it.

For software, that means translatability as a structural property of the codebase, not a feature added later. Cybersecurity and data compliance requirements vary across geographies in ways that are genuinely hard

to retrofit. For hardware, cost expectations, manufacturing considerations, and certification requirements vary by market. Meeting North American standards does not mean meeting the next market’s standards. Sometimes it requires real redesign, not relabelling.

The architectural decisions that look like overhead in early build are often exactly why expansion does not require starting over. Founders who understood that early saved years.

The people on the ground are the product

Healthcare workflows are not the same everywhere. How a product gets purchased, approved, reimbursed, and adopted varies by geography in ways that only local expertise can navigate.

Local product managers and regulatory specialists are not a later-stage hire. They are what makes expansion actually work. For companies not ready to commit to full-time local staff, employer of record services are a lower-risk way to place people in a new market while you figure out your footing.

You cannot run an international expansion from headquarters.

The part at the end that was worth staying for

The operational conversation ran most of the session. Then, near the close, it got more personal. Several speakers talked about what it had taken to get to the table and stay there. Finding mentors who became real allies. Turning off the voice that says you cannot. Taking bigger risks than felt comfortable.

“Find your voice. Lean in.”

Simple. But it landed because the people saying it had earned the right to say it.

Going global is not a clean process. It is legally complicated, financially surprising, and deeply dependent on people and relationships that take time to build. The founders who do it well are not the ones who move fastest. They are the ones who asked the right questions early and built structures that could hold the weight of what they were building toward.

FOUNDER’S NOTE

What I keep thinking about is how much of the hard stuff in building a company is not secret. It is just not talked about until you are already inside it. Legal structure feels like admin until it is a constraint. Investor relationships feel transactional until they are governance. Expansion feels like a distribution challenge until it is clearly a product one. The gap between the lab and the boardroom is real, and the earlier you understand what is in it, the better your chances of crossing it.

That is why conversations like this one are worth documenting. The people in that room had earned their answers. And they were generous enough to share them before anyone had to learn the hard way.

Leave a Reply