Most fundraising conversations center on the “yes.” The term sheet, the close, the announcement are the moments everyone prepares for, talks about, and celebrates. What gets far less attention, and far less preparation, is everything that happens around the “no.” A small word, but one that holds so much power.

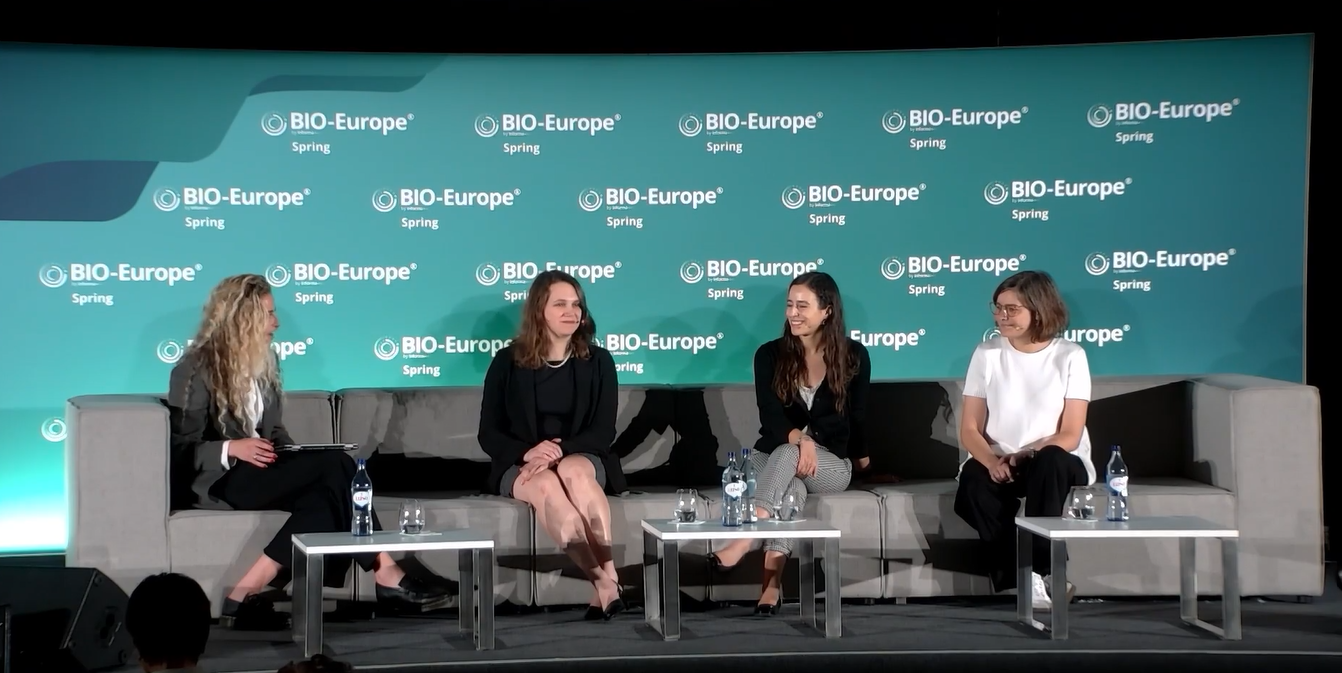

At BIO Europe Spring in Lisbon, a panel titled “The Art of Drawing Back: Why Founders and Investors Sometimes Say No” brought together an executive director from a corporate venture arm, a managing partner from an independent life sciences fund, and a founder-CEO building in cell fate reprogramming. Their moderator opened with a frame that set the tone for the hour.

“Saying no is often just as important and often much harder for founders.”

The conversation that followed covered decision frameworks, the pressure of thematic hype cycles, what separates useful feedback from a vague pass, and why optionality is a CEO’s job.

Why “No” Is a Strategic Decision

For investors, a pass isn’t simply an absence of interest. It can mean timing is off, the portfolio already has exposure in that area, or the evidence isn’t there yet. The reason matters, and so does how it gets communicated.

Corporate VCs play by different rules. They tend to prefer companies that are further along and have a defined path to a product. They also have to ask whether your work fits what their parent company is already doing. A regular VC doesn’t have to think about that. If you’re pitching a corporate VC, it helps to understand that going in.

“If I don’t say no to some of these opportunities… I can’t work even more deeply with the ones that I can work with.”

How Decision Frameworks Evolve

All three panelists noted a shift in what they weight over time. Early in a career, novelty and scientific rigor tend to dominate. With experience, the question becomes: can this team actually build something?

“We back people just as much as we back science.”

Who else is in the round matters too. Investors think about who they’ll be sitting across a board table from for years. Every funding round has a group of co-investors, called a syndicate, and who is in that group shapes a company’s trajectory as much as who owns what percentage of it.

Thematic Waves and the FOMO Problem

Biotech moves in cycles. Cell therapy, gene editing, AI drug discovery, GLP-1 adjacencies. When a category heats up, money pours in. It gets harder to stand out, and investors become more skeptical of companies that sound like every other pitch they’ve seen.

The panelists said they try to spot trends early so they’re not scrambling to invest once a space gets hot. By the time a category is crowded, a fund may simply not have room for another company in that area, no matter how good it is. That’s not a comment on your science. It’s just a math problem on their end. Founders should know the difference.

For founders navigating a saturated category, the question strays away from how to sound different. It’s how to demonstrate a genuinely distinct mechanism, patient population, or clinical strategy. The founder on the panel had constrained her company’s scope deliberately, combining two areas, cell reprogramming and immunology, to stake out her own lane, separate from the neuron and heart-focused work that had defined the field. Scope constraints were a competitive decision, not a limitation.

The Mechanics of a Good “No”

The panelists converged on a few practices that separate a constructive pass from a damaging one.

Speed

Respond within one to two weeks. Founders making operational decisions around a fundraise cannot wait months for a signal that was never coming.

Universality

“Answer to everyone. That’s a must within our company.”

Specificity

When the reason for passing is communicable, share it. An investor’s view is just one opinion. It’s not a final ruling. Sharing it with appropriate humility respects the founder’s expertise and leaves the relationship intact.

Open Doors

CVCs may be constrained in what they can disclose. But the door should stay open for meaningful data updates, pivots, or shifts in strategic priority. A no today isn’t necessarily a no at Series B.

The Founder’s Side of the Conversation

“My role as CEO and manager is to bring optionality.”

More options make it possible to choose the right partner rather than the available one. A founder with only one serious investor isn’t negotiating. They’re just taking what they can get.

Founders on this panel said they prefer a clear, decisive no when there is no fit. Ambiguity is expensive. When partial alignment exists but timing or structure is off, detailed feedback is valuable. That feedback, even when it initially stings, is data for the next conversation.

“It’s never personal… it’s always around where it fits into our perspective.”

The No Framework: What Each Side Owes the Other

| FOR INVESTORS | FOR FOUNDERS |

| Respond within 1 to 2 weeks | Treat optionality as a CEO responsibility |

| Reply to everyone, not just likely deals | Ask for specific feedback when partial fit exists |

| Name the real reason when you can | Distinguish a structural pass from a scientific one |

| Hold the humility that your view is one opinion | Use declines to refine story and improve fit |

| Monitor portfolio balance to avoid last-minute pressure | Protect core vision while iterating on framing |

| Keep doors open when timing is the issue | Evaluate the syndicate, not just the lead |

On Syndicate Dynamics and Internal Dissent

One of the more candid moments in the panel addressed what happens inside a VC firm before a yes is reached.

“You need someone within that VC firm that is going to fight for your company and for your deal, but you also want the team to be comfortable enough to challenge you.”

A deal that faces no internal friction often hasn’t been examined hard enough. Founders should know that pushback inside a VC firm isn’t opposition. It’s just the team doing their homework. A champion who survives that process is a more reliable board ally than one who sailed through unopposed.

The most durable relationships in biotech span multiple companies and many years. How a “no” is delivered shapes whether that relationship survives the pass. Founders and investors who treat declines as strategic decisions rather than personal rejections build the kind of networks that pay forward long after any single deal.

That is the actual art of saying no. Not the words, but what you preserve by choosing them carefully.

Leave a Reply